#central-bank-rates

#central-bank-rates

[ follow ]

#inflation #interest-rates #federal-reserve #monetary-policy #bank-of-england #energy-prices #us-dollar

#inflation

US politics

fromFortune

4 days agoJerome Powell lets loose: 'it's very hard to build great democratic institutions and much easier to bring them down' | Fortune

Monitoring inflation is crucial due to energy price spikes, while the job market remains challenging for young graduates amid AI advancements.

US politics

fromFortune

4 days agoJerome Powell lets loose: 'it's very hard to build great democratic institutions and much easier to bring them down' | Fortune

Monitoring inflation is crucial due to energy price spikes, while the job market remains challenging for young graduates amid AI advancements.

#us-dollar

US Elections

fromLondon Business News | Londonlovesbusiness.com

2 days agoUS dollar rose amid a rebound in geopolitical concerns - London Business News | Londonlovesbusiness.com

The US dollar strengthened due to geopolitical fears and better-than-expected economic data, while uncertainty keeps market volatility high.

US Elections

fromLondon Business News | Londonlovesbusiness.com

2 days agoUS dollar rose amid a rebound in geopolitical concerns - London Business News | Londonlovesbusiness.com

The US dollar strengthened due to geopolitical fears and better-than-expected economic data, while uncertainty keeps market volatility high.

from24/7 Wall St.

1 day agoHow Income Investors Are Using HYBL to Dodge Interest Rate Risk in 2026

HYBL attempts to solve the income problem by combining senior loans, high-yield corporate bonds, and debt tranches from U.S. collateralized loan obligations (CLOs). The result is a portfolio with lower duration and lower volatility compared to traditional high-yield funds, while still targeting high current income with monthly distributions.

Business

fromIndependent

1 day ago'If you are using credit cards to take out cash, you need to cut up your card' - money experts share their credit card dos and don'ts

Credit cards can be very dangerous from a financial well-being perspective, if used irresponsibly. The temptation to use one to fund a big holiday or a new sofa that you can't afford can be seriously tempting.

Relationships

#geopolitical-risk

UK news

fromLondon Business News | Londonlovesbusiness.com

3 weeks agoExpectations for UK interest rate cuts shift dramatically - London Business News | Londonlovesbusiness.com

Geopolitical tensions are pushing markets toward higher interest rates and oil prices, benefiting energy and defence sectors while shifting investment away from growth stocks.

Retirement

fromLondon Business News | Londonlovesbusiness.com

1 day agoEvery time you borrow from a bank, you're paying more than you think - London Business News | Londonlovesbusiness.com

Opportunity cost in loans includes lost potential earnings from repayment dollars, not just the interest rate paid.

#bank-of-england

UK news

fromLondon Business News | Londonlovesbusiness.com

1 month agoBank of England pressed to 'cut interest rates and prioritise growth' - London Business News | Londonlovesbusiness.com

High interest rates are suppressing investment, spending and growth; the Bank of England must cut rates now or risk economic stagnation and job losses.

Artificial intelligence

fromFortune

3 days ago'Inflationary surge': Fed economists warn AI hype is overheating the economy whether or not the technology ever delivers | Fortune

AI optimism may hinder productivity and contribute to short-term inflation as households and businesses react to perceived future gains.

World politics

fromwww.theguardian.com

3 days agoA third inflationary shock in less than a decade is coming: who will pay the price this time around? | Aditya Chakrabortty

Daniel Yergin highlights the vulnerability of global oil supplies through the Strait of Hormuz and the consequences of military actions against Iran.

from24/7 Wall St.

4 days agoXRP Price Prediction: What Happens to XRP If Oil Stays Above $100 and the Fed Doesn't Cut?

XRP has had the strongest fundamental setup of any altcoin in 2026—a commodity classification from both the SEC and CFTC, seven ETFs with $1.44 billion in inflows, and major partnerships with Mastercard and Deutsche Bank.

Cryptocurrency

fromwww.mediaite.com

5 days agoBad News All Around!' Fox Business Host Stunned By Highly Inflationary' Prices in Total Bummer of an Economic Analysis

High energy prices are kryptonite for the housing market. Affordability, especially for those first-time home buyers, is now an elusive dream until oil prices come down and interest rates come down.

SF real estate

#gbpusd

UK news

fromLondon Business News | Londonlovesbusiness.com

4 days agoCautious recovery for the British pound after consecutive losses near $1.31 - London Business News | Londonlovesbusiness.com

Geopolitical risks now dominate GBP/USD movements, overshadowing traditional economic factors and creating volatility in the currency pair.

#eurusd

Europe news

fromLondon Business News | Londonlovesbusiness.com

1 week agoEuro rally falters as dollar regains strength on 'higher for longer' rates - London Business News | Londonlovesbusiness.com

EURUSD recovery shows fading momentum, reflecting a corrective rally rather than a trend reversal amid complex macroeconomic conditions.

Europe news

fromLondon Business News | Londonlovesbusiness.com

1 week agoEuro rally falters as dollar regains strength on 'higher for longer' rates - London Business News | Londonlovesbusiness.com

EURUSD recovery shows fading momentum, reflecting a corrective rally rather than a trend reversal amid complex macroeconomic conditions.

fromFortune

5 days agoBond yields are falling even as oil tops $102, showing that Wall Street fears recession more than inflation | Fortune

"Oil prices are higher again this morning, but Treasury yields are lower as the risks to economic growth begin to take precedence over the risks to inflation," Oxford Economics said in a note on Monday.

World news

from24/7 Wall St.

2 days agoJPMorgan's Short-Duration JPIE Earned 15.24% Since Inception While the Bond Market Cratered

JPMorgan Income ETF has delivered over 50 consecutive monthly distributions since its October 2021 inception, providing stability that is the entire point of the investment strategy.

Business

World politics

fromLondon Business News | Londonlovesbusiness.com

5 days agoUS dollar stable after successive gains - London Business News | Londonlovesbusiness.com

Escalating Middle East tensions are influencing market sentiment, keeping the dollar stable and impacting US Treasury yields amid inflation concerns.

US Elections

fromAxios

2 weeks agoFed keeps rates on hold, Powell says he will remain in place until successor confirmed

Powell commits to remaining at the Federal Reserve through a criminal investigation into his leadership, blocking his successor's confirmation and resisting Trump administration pressure to lower interest rates.

from24/7 Wall St.

3 days agoWall Street Bullish on Americas Gold and Silver: BMO Sees Major Re-Rate Ahead

BMO believes Americas Gold has the expertise to execute its optimization strategy, particularly at the Galena Complex, and sees the company's approach increasing free cash flow generation as production grows organically.

Business

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoEurozone inflation edges up as ECB prepares for key rate decision - London Business News | Londonlovesbusiness.com

Services experienced the highest annual increase at 3.4%, followed by food, alcohol, and tobacco at 2.5%. Non-energy industrial goods saw a more modest increase of 0.7%. Meanwhile, energy prices fell by 3.1% over the month, which helped to temper overall inflation pressures.

Europe news

Business intelligence

from24/7 Wall St.

4 weeks agoThe Last Time the Fed Chair Was This Hawkish, the Market Did Something Surprising

Institutional investors show cautious restraint as elevated market uncertainty persists alongside a hawkish Federal Reserve maintaining high interest rates and persistent inflation trends.

UK news

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoBank of England holds base rate amid Middle East war - London Business News | Londonlovesbusiness.com

The Bank of England held the base interest rate at 3.75% due to Middle East conflict uncertainty and rising energy prices threatening inflation expectations.

#uk-interest-rates

UK news

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoUK rates: Savers, investors should act now in higher-for-longer era - London Business News | Londonlovesbusiness.com

UK interest rates will likely remain elevated longer than expected due to renewed inflation threats from energy prices and geopolitical tensions, requiring savers and investors to adjust their financial strategies accordingly.

fromLondon Business News | Londonlovesbusiness.com

2 weeks agoDollar retreats ahead of federal reserve interest rate decision - London Business News | Londonlovesbusiness.com

The dominant force in play remains the Middle East conflict, which has kept oil prices elevated and inflation expectations firm. Reports that Washington is assembling a coalition to escort vessels through the Strait of Hormuz could offer some relief for the oil market and could weigh on the dollar.

World news

fromLondon Business News | Londonlovesbusiness.com

3 weeks agoDollar under pressure as geopolitical concerns ease - London Business News | Londonlovesbusiness.com

The expectations of a decrease in tensions triggered a pullback in oil prices, which in turn softened immediate concerns about inflation pressures. However, the broader geopolitical backdrop remains fragile, and any renewed escalation could quickly push oil prices, the dollar, and Treasury yields higher again.

World politics

US news

fromLondon Business News | Londonlovesbusiness.com

1 month agoDollar Relatively Stable Amid Economic Uncertainty - London Business News | Londonlovesbusiness.com

The dollar remains stable within a consolidation range, with its direction dependent on monetary policy expectations, labor market data, and inflation trends.

Business

fromSilicon Canals

1 week agoGold crossed $5,300 the same week three central banks quietly dumped $47B in US Treasuries. That's not coincidence - it's coordination - Silicon Canals

Gold's price surge is driven by strategic positioning of central banks, not just fear, as they reduce US Treasury holdings amid geopolitical tensions.

from24/7 Wall St.

4 weeks agoInterest Rates Are Heading Down - These 3 Stocks Win Big When They Do

In my view, interest rates are more likely than not going to head lower over the course of 2026 and into 2027. I'm not saying we're due for a pandemic-like selloff, but I do think that weakness in the labor market is likely more protracted than the government data suggest. As such, I do think the makeup of the Federal Reserve, and which way many of its presidents and voting members lean (toward providing support for the labor market over battling inflation) could lead to much faster rate cuts than many think.

Retirement

fromLondon Business News | Londonlovesbusiness.com

3 weeks agoDollar surges on geopolitical risks and rising yields

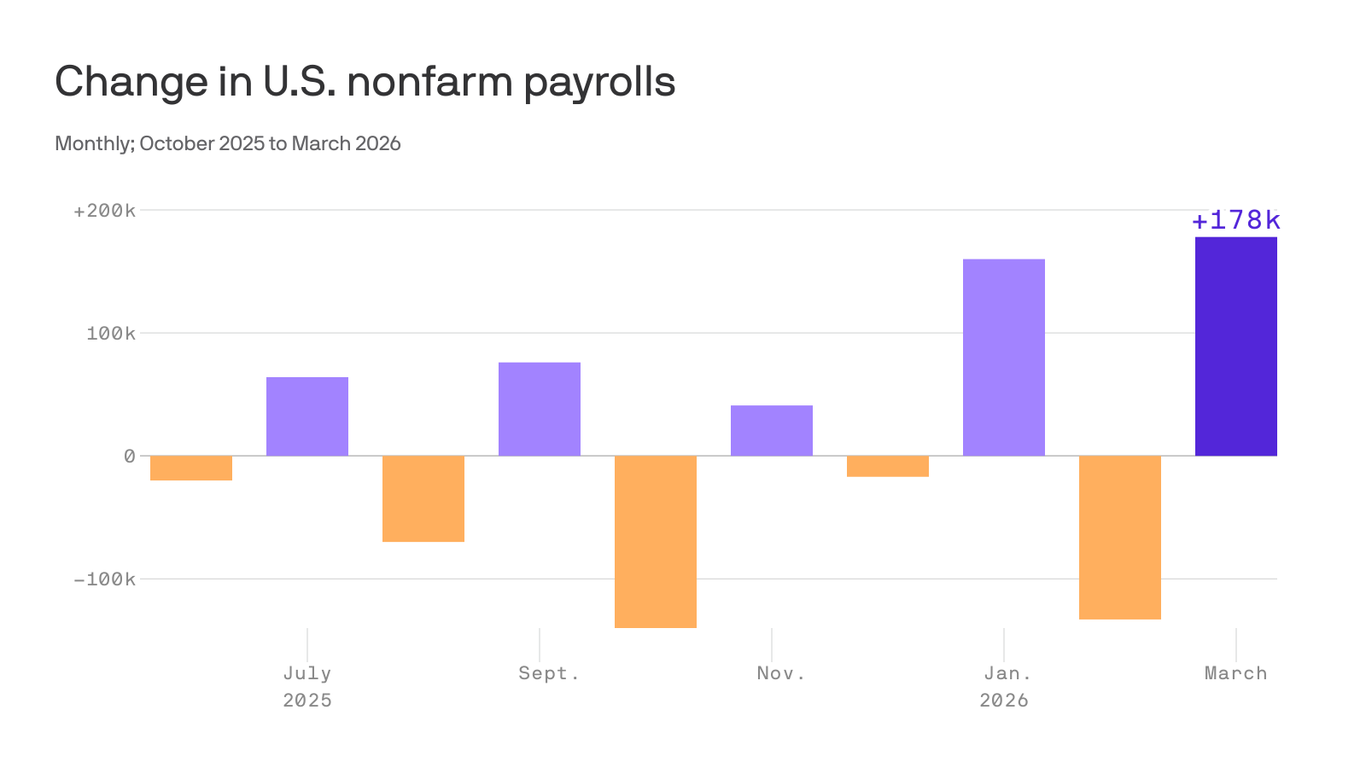

Crude oil breaking above the USD 100 threshold has revived inflation concerns, pushing US Treasury yields higher across the curve. However, Friday's labour market report revealed a significant deterioration in employment conditions, with the economy losing 92,000 jobs in February, its largest contraction in several months.

World news

World politics

fromLondon Business News | Londonlovesbusiness.com

1 month agoThe Euro Could Head Closer to Unity with the Dollar - London Business News | Londonlovesbusiness.com

EUR/USD declines toward parity as energy crisis concerns and rising eurozone inflation pressure the euro while US Treasury yields support dollar strength.

Business

fromwww.housingwire.com

2 weeks agoFed holds rates, officials signal wait and see on inflation risks

Oil price resolution timing in the Strait of Hormuz will determine whether inflation stays elevated, delaying Fed rate cuts, or eases, allowing Treasury yields and mortgage rates to decline toward early-year levels.

fromBusiness Matters

1 month agoBank of England rate cuts at risk in 2026 as Middle East conflict sparks inflation fears

With 2-year gilt yields hitting December highs due to a 40 per cent surge in UK gas prices and oil nearing $80, the Bank of England faces a significant inflationary shock. High-street banks are no longer competing on price but are instead protecting margins against rising swap rates.

UK news

from24/7 Wall St.

1 month ago3 ETFs to Buy ASAP Before Jerome Powell's Term Ends in May

Warsh served on the Fed's Board of Governors from 2006 to 2011, making him the youngest person ever appointed to that role at age 35. During the 2008 financial crisis, he was part of Ben Bernanke's inner circle and served as an intermediary with Wall Street. He negotiated survival plans for firms like Morgan Stanley (NYSE:MS). He later resigned from the Fed due to disagreements over its balance sheet expansion policies.

US politics

fromLondon Business News | Londonlovesbusiness.com

1 month agoDollar struggle and monetary policy shape the next phase - London Business News | Londonlovesbusiness.com

The resilience of gold above $4,800 per ounce at this stage reflects a delicate and complex balance between traditional supporting factors and emerging pressures-one that cannot be superficially interpreted or reduced to the movement of the dollar alone. It is true that the U.S. dollar's retreat from its recent peaks, after failing to sustain its recovery momentum from a four-year low, provided gold with a short-term breather and attracted some buyers.

Business

Business

fromLondon Business News | Londonlovesbusiness.com

1 month agoGold declined on cautious Fed members' comments - London Business News | Londonlovesbusiness.com

Gold prices fell as a stronger US dollar and cautious Fed signals pressured non-yielding assets, while geopolitical tensions could cap further declines.

[ Load more ]